MCMC sampling for Bayesian quantile regression. An asymmetric Laplace distribution is assumed for the errors, so the regression models targets the specified quantile. A g-prior is assumed for the regression coefficients.

Usage

bqr(

y,

X,

tau = 0.5,

X_test = X,

psi = length(y),

nsave = 1000,

nburn = 1000,

nskip = 0,

verbose = TRUE

)Arguments

- y

n x 1vector of observed counts- X

n x pmatrix of predictors (no intercept)- tau

the target quantile (between zero and one)

- X_test

n_test x pmatrix of predictors for test data; default is the observed covariatesX- psi

prior variance (g-prior)

- nsave

number of MCMC iterations to save

- nburn

number of MCMC iterations to discard

- nskip

number of MCMC iterations to skip between saving iterations, i.e., save every (nskip + 1)th draw

- verbose

logical; if TRUE, print time remaining

Value

a list with the following elements:

coefficientsthe posterior mean of the regression coefficientsfitted.valuesthe estimatedtauth quantile at test pointsX_testpost_theta:nsave x psamples from the posterior distribution of the regression coefficientspost_ypred:nsave x n_testsamples from the posterior predictive distribution at test pointsX_testpost_qtau:nsave x n_testsamples of thetauth conditional quantile at test pointsX_testmodel: the model fit (here,bqr)

as well as the arguments passed

Note

The asymmetric Laplace distribution is advantageous because

it links the regression model (X%*%theta) to a pre-specified

quantile (tau). However, it is often a poor model for

observed data, and the semiparametric version sbqr is

recommended in general.

An intercept is automatically added to X and

X_test. The coefficients reported do *not* include

this intercept parameter.

Examples

# Simulate some heteroskedastic data (no transformation):

dat = simulate_tlm(n = 100, p = 5, g_type = 'box-cox', heterosked = TRUE, lambda = 1)

y = dat$y; X = dat$X # training data

y_test = dat$y_test; X_test = dat$X_test # testing data

# Target this quantile:

tau = 0.05

# Fit the Bayesian quantile regression model:

fit = bqr(y = y, X = X, tau = tau, X_test = X_test)

#> [1] "1 sec remaining"

#> [1] "1 sec remaining"

#> [1] "Total time: 0 seconds"

names(fit) # what is returned

#> [1] "coefficients" "fitted.values" "post_theta" "post_ypred"

#> [5] "post_qtau" "model" "y" "X"

#> [9] "X_test" "psi" "tau"

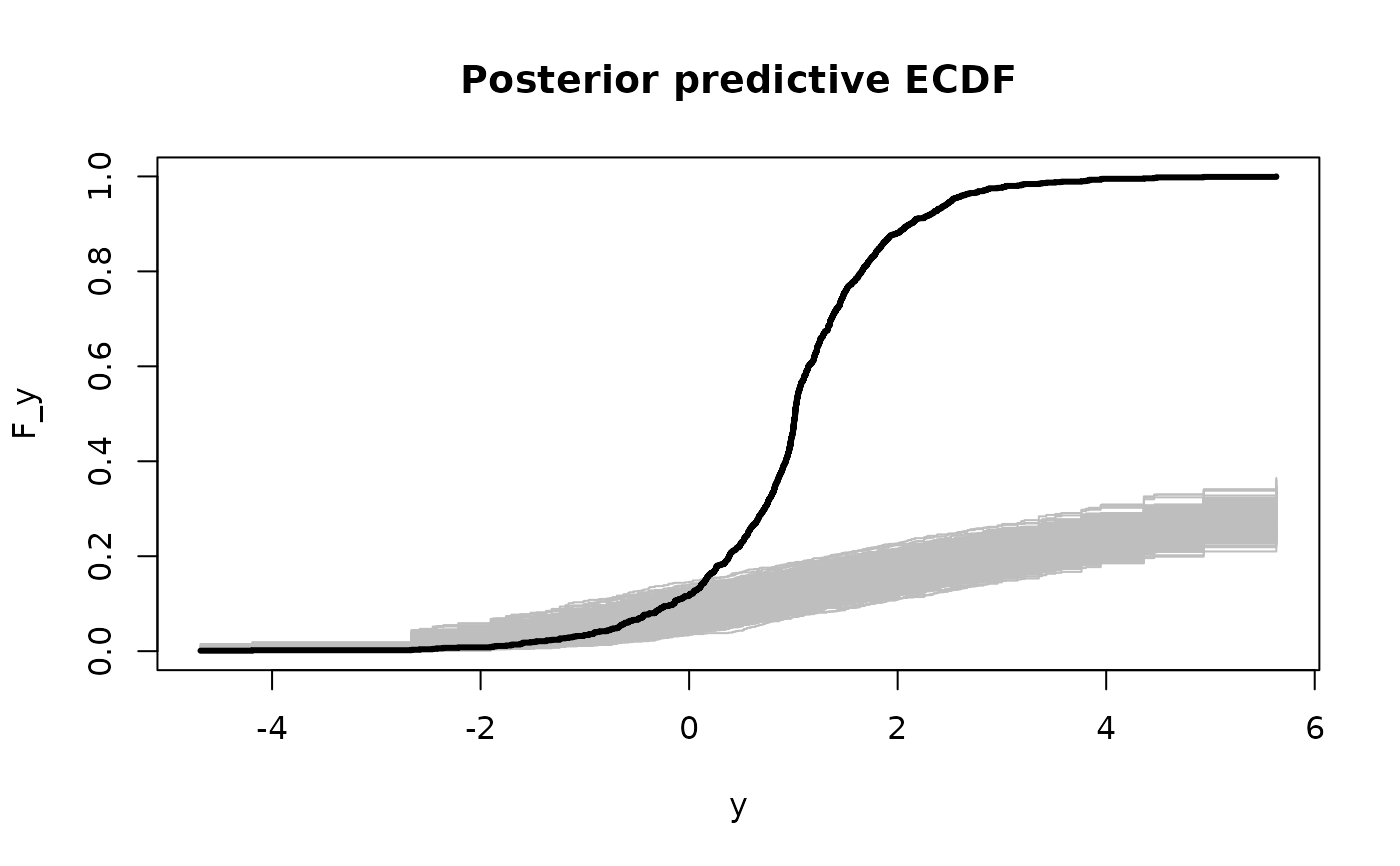

# Posterior predictive checks on testing data: empirical CDF

y0 = sort(unique(y_test))

plot(y0, y0, type='n', ylim = c(0,1),

xlab='y', ylab='F_y', main = 'Posterior predictive ECDF')

temp = sapply(1:nrow(fit$post_ypred), function(s)

lines(y0, ecdf(fit$post_ypred[s,])(y0), # ECDF of posterior predictive draws

col='gray', type ='s'))

lines(y0, ecdf(y_test)(y0), # ECDF of testing data

col='black', type = 's', lwd = 3)

# The posterior predictive checks usually do not pass!

# try ?sbqr instead...

# The posterior predictive checks usually do not pass!

# try ?sbqr instead...